Click here to read the monthly eNewsletter exclusive for BlueRocke clients:

https://bluerocke.com/wp-content/uploads/2023/06/BlueRocke-June-Newsletter.pdf

BlueRocke Monthly Client Newsletter – April

Click here to read the monthly eNewsletter exclusive for BlueRocke clients:

https://bluerocke.com/wp-content/uploads/2023/04/BlueRocke-April-Newsletter.pdf

BlueRocke Monthly Client eNews

Click here to read the monthly eNewsletter exclusive for BlueRocke clients:

How to build wealth in your 30s

Key takeaways

- Investing with a long-term plan means you’re less likely to be affected by short-term market fluctuations

- Keeping track of your expenses versus income can help identify possible savings to pay off debt

- Adding more to your super on a regular basis offers tax benefits in addition to improving your retirement.

To all the thirty-somethings out there, now’s your time to shine! These are the years that will shape the rest of your life.

If you’re looking for a bright future—that’s not held back by financial worry—here’s four simple tips to start building wealth now so you can chill later.

1. Consider long-term investing

Having time on your side—one of the great benefits of being in your 30s—can mean a great deal in the investing world.

Why? If you invest with a long-term plan, you’re less likely to be affected by short-term volatility.

With growth assets like shares and property, your chance of a negative return gets lower the longer you invest. In your 30s you’re in a better position to use that pattern to your advantage – to take on more risk to generate higher returns, if you choose to.

Shares

Generally speaking, shares outperform many other investments over the long term.1

There’s also the benefit of dividends. If you invest in companies that pay dividends, you’ll benefit from part of the company’s profits paid to shareholders (generally twice a year). That can be handy income – or reinvested to keep growing your capital.

Property

Owning an investment property may be another way to generate a good income stream – with tenants paying you rent. This income may also help to pay off your mortgage so you can capitalise on another investment later in life.

Like shares, Australian residential property has delivered strong long-term returns.2 While less volatile than shares, it’s important to note property values do change depending on supply and demand in the market.

2. Seek help from a professional

If you value the experience of experts in other aspects of your life, don’t discount it when it comes to managing your life savings.

A financial adviser is not just someone who helps with investments. Their job is to help you with every aspect of your financial life—savings, insurance, tax, debt—while keeping you on track to achieve your goals.

More importantly, they can answer questions like:

- How can I pay off my mortgage faster and reduce my debt?

- What strategies can I use to build my wealth?

- What age can I stop working and retire?

If your to-do list is endless and you never quite have time to tackle your personal finances, a financial adviser may help to set you on the right track.

3. Gain control of your debt

Debt management is a crucial skill when it comes to managing money, saving and planning for the future.

Whether it’s a credit card, personal loan or a mortgage you’re paying off, setting priorities and keeping track of your expenses/income to identify potential savings may help to pay off debts sooner. And the sooner you pay off your debts, the more money you can invest for a better lifestyle in future.

Set priorities

If you have more than one outstanding debt, consider working out how much you can repay on each, based on the minimum repayment owing.

Alternatively, if you’re able to repay more than the minimum, look at prioritising your debts. You’ll need to think about the type of debt you have—an investment loan or personal debt—and how much is owing. If you only have personal debt, you could prioritise repaying debts with the highest interest rate first, given these will be costing you the most.

Keep track of expenses and income

Having a clear picture about what you earn versus what you spend can highlight areas where you could save more. Whatever income you’re able to save can then be allocated towards your debt.

There are budget planners and phone apps you can use to track your spending. Alternatively, you can simply download your bank statements and keep a record of your receipts.

4. Add more to your super

Super is one way to generate wealth over the long-term due to compounding returns. Compound returns is the way your balance increases if you give your investment time for the growth you got this year to grow again next year – and the year after that and the year after that.

In your 30s you’ve got time to get compound returns on your side. One way to maximise this benefit is to contribute more into your super on a regular basis. You can do this using your before or after-tax income and there may be tax benefits that come with this too.

For example, if you contribute some of your after-tax income or savings into super, you may be eligible to claim a tax deduction.

Be mindful of contribution caps though. They limit the amount of super contributions you’re able to make each year if you want to avoid paying tax at your marginal tax rate rather than the concessional rate of

15%.

If you have questions and would like your financial situation to be evaluated, please email us on ds@bluerocke.com with your contacts, for an exploratory meeting, at our cost, not yours.

Article Source: https://www.mlc.com.au/personal/blog/2020/12/how_to_build_wealth_in_your_30s

The power of compound interest

Albert Einstein is reputed to have said: “Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.”

As an investor, making your money work for you is the best way to increase your wealth. And the wealth you will accumulate is the result of 2 things: how long you invest and the rate of return on your investment.

You will also need psychological qualities to make the whole thing work. Qualities like being patient, disciplined, knowing the value of things, and being able to act decisively on your own reasoning (and not on the opinion of others) when the odds are in your favour.

Doing the maths

Why is compound interest so “magical”? The simple answer is: “Because it’s reinvested”. Compound interest is, simply put, interest on interest.

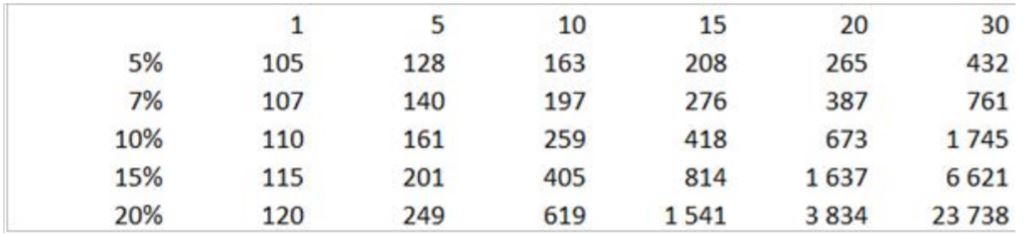

Here’s an example. Assume you invest $100. The following table shows how much return you’d get over different lengths of time, and at varying rates of return.

The power of compounding – in a table

If you invest $100 at 5% over 5 years, you get $128, but if you wait 10 years, that amount rises to $163. The longer you wait, the more you make! Of course, this goes even higher if you can get a higher return. For example, if you can find an investment that returns 15% for 10 years, you multiply your money by a factor of 4. If you wait for 20 years and still earn 15% a year (which is a lot), you get 16 times your money back.

Twenty-percent seems like a very high unachievable return. Actually, it’s pretty rare, reserved to the most talented investors, such as Warren Buffett (the annual return of per-share market value of Berkshire Hathaway has been 20% per annum, over 55 years…).

Two factors to remember

If you want to accumulate wealth, you will need to start as early as possible and then focus on the best prospective return you can find.

The second factor is obviously the most difficult to get, because it depends on careful study of key elements such as the price you pay for the assets in which you invest, and their intrinsic qualities.

For instance, if you want to invest your money in stocks, you will need to select individual companies that boast high quality, and that trade at cheap valuation.

High quality companies are companies that have a strong competitive position in their market, have growth in their industry, generate high return on capital and growing free cash-flow, a strong balance sheet, and are managed by competent people.

You can’t control the market

Cheap valuation is also not an element you control. It’s usually the reflection of other people’s opinion, aka “Mr. Market”, that sometimes agrees to pay a lot for a company and at other times is willing to sell at a huge discount (per Benjamin Graham’s real quote in his must read book The Intelligent Investor or those quotes from Warren Buffett in his 1987 letter to shareholders).

But if you’re patient enough and know which companies/assets you want to buy, you just have to be patient and wait for the market to provide the opportunity to buy something you like at a fair price.

Then you will just have to stick to your guns and wait for other opportunities to come along.

If you have questions and would like your financial situation to be evaluated, please email us on ds@bluerocke.com with your contacts, for an exploratory meeting, at our cost, not yours.

Article Source: https://spotlight.morningstarhub.com.au/the-power-of-compound-interest/?utm_source=eloqua&utm_medium=email&utm_campaign=thought_leadership_research&utm_content=31686

What qualified advisers have over “finfluencers”

More people than ever are taking control of their money – but where do they go if they’re after financial advice? While ‘finfluencers’ are appealing to younger investors, ensuring any advice comes from a qualified adviser gives you a better chance of meeting your goals.

Since the pandemic began, more people have become interested in investing, particularly in the share market. Research house Investment Trends found about 435,000 new investors bought shares for the first time in 2020 and of these 18 per cent were aged less than 25, while 49 per cent were between 25 and 39. This influx of investors brings a new challenge – that of educating this group on investment strategies. So, where should they go for advice?

Generally, if an investor wants advice, they seek out a financial adviser. A report into financial advice highlights demand for advice has doubled over the past five years. It found three out of four advised clients engaged with their adviser during lockdown while 2.6 million non-advised Australians said that they intended to seek advice. This demonstrates an increase in awareness of how valuable financial advice is. Other research backs this up. Rice Warner’s 2020 report – Future of Advice – found those who receive advice accumulate 3.9 times more assets after 15 years than those who make their own decisions.

The rise of the ‘finfluencer’

However, not everyone is going to a qualified financial adviser to discuss their financial needs. Over the past few years, financial influencers or ‘finfluencers’ have emerged, dispensing (often questionable) advice via social media platforms. Described as social media content creators that build audiences through providing financial advice, finfluencers can be found on platforms such as TikTok, YouTube, Twitter, Instagram and Reddit. But should people be taking their advice?

Some finfluencers have shown their audiences take quite a lot of notice of them. For example, the number of trades in the US video game retailer Gamestop took off after it was pumped on Reddit and tweeted about by Tesla founder Elon Musk. But it’s a case of buyer beware with these unlicenced and mostly unqualified sources. In fact, the Australian Securities and Investments Commission has been dealing with rising numbers of complaints relating to unlicensed financial advice since March 2020 – when the pandemic began.

But while the advice of some finfluencers may be suspect, they do appeal to a particular audience – such as Millennials and Gen Z. There are also some finfluencers who appear to help people better engage with their finances. But while finfluencers can provide useful tips on how to save or budget, sharing investment tips and strategies is where inexperienced investors need to take care. It’s important to be very wary of investment advice, especially if someone is pushing a scheme that they benefit from personally.

Why a qualified financial adviser?

While a finfluencer doesn’t need to have any particular expertise (and often doesn’t), anyone giving financial advice must hold an Australian Financial Services Licence (AFSL) or be acting as an authorised representative of an AFS licensee. Anyone wanting to become a financial adviser must also complete a full-time professional year that includes at least 100 hours of structured training.

If you’re serious about building your wealth and meeting your financial objectives, a qualified financial adviser whom you can build a relationship with over time, is the best person to provide you with the advice that will guide you at every life stage.

So how does financial advice help investors? Some of the areas an adviser can help with include:

- Setting financial goals

- Advising on wealth-building strategies to meet your goals

- Advising on appropriate insurance to protect your health, wealth and family

- Estate planning

The benefits of seeking advice are many. An IOOF paper – The True Value of Advice – reveals the long-term benefits that financial advisers provide, with 90 per cent of advised clients surveyed saying that accessing financial advice has left them in a better position financially and 89 per cent reporting that receiving advice allowed them to live their desired lifestyle.

It’s also important to remember that financial advice is not just for those nearing retirement. Seeking advice early on could make a big difference to your finances at all stages of your life, such as when you’re buying a property, starting a family, or wanting to access your superannuation.

If you have questions and would like your financial situation to be evaluated, please email us on ds@bluerocke.com with your contacts, for an exploratory meeting, at our cost, not yours.

Article Source: http://www.onepath.com.au/investor-insights/news/news-what-qualified-advisers-have-over-finfluencers.aspx