In this 3 minute video, MLC’s Brendan Johnson discusses the role of good financial advice during COVID-19 and how clients want to build confidence and a sense of control in this extraordinary time.

We are here to help, contact Dev Sarker at 1300 7171 136 today.

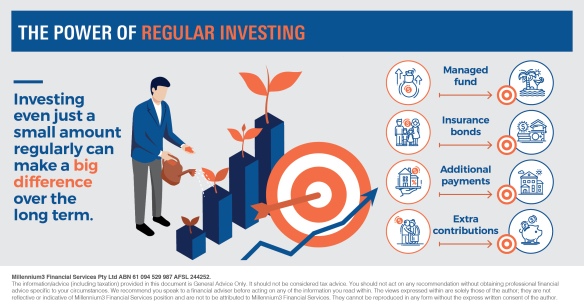

If you want to get ahead, financially, it’s necessary to take some steps to get there. It may seem daunting and overwhelming but like anything, if you have a professional guiding you along the way, small steps can lead to something great.

Step 1 | Seek advice

It’s hard to achieve great success without a team of experts behind you and your wealth is no different. Getting professional financial advice means your adviser can work through a myriad of options with you and implement a strategy aligned closely to your financial goals. Retirement planning, tax-effective super strategies, investments and estate planning? Your financial adviser can help.

Step 2 | Understand what role risk plays

One of the first things your financial adviser will do is work out your risk profile, which they will check at regular review meetings. Why? Because risk is related to return, and this will help drive the recommendations they make to you in terms of your financial plan. Generally, the higher the risk, the higher the return. While some people like higher risk investments because they have the potential to deliver higher returns, others prefer less risky investments. It’s important to remember that markets are cyclical and shares are a long-term investment so if the market wobbles, your financial adviser is best placed to keep an eye on your investments and determine if they remain aligned to your overall financial strategy.

Step 3 | Check your super

Your superannuation could be your largest asset, other than your own home. Given it’s such a large sum that you have been contributing to for years and years, and you are relying on it to sustain you in your retirement, isn’t it something you want to get right? Sure, it’s a long-term investment, but it’s important that it is invested in-line with your risk profile and financial goals. And you DO have options. As well as your employer contribution, you can kick in a bit extra through salary sacrificing. Contributing more to super will not only boost your account balance, it could reduce the amount of tax you pay.

Step 4 | Stick to a budget

Sounds boring, right? But a budget is not boring, it’s empowering!! Setting a realistic budget helps you understand where your money is going, what can be trimmed and where you can invest to save for your future. Understanding your overall financial health and having a budget aligned to your financial goals gives you a real understanding of the benefits of working with a financial adviser. You can start to see a real change in your circumstances. Having a budget doesn’t mean giving up things you want, it just means you plan for them and you make sure you can afford them BEFORE you spend the money. Setting and sticking to a budget is really the simplest way to help you get ahead.

Need advice? We’re happy to help. Call 1300 71 71 36 to speak to a financial adviser today!

Are you asset rich but cash poor? You’re not alone. Data from the Australian Bureau of Statistics shows that almost one-third of older Australians in low-income households were asset rich but cash poor.[1] Most of their wealth was tied up in illiquid assets, in particular their home.

But you need not scrape by on so little. There are ways to try boost your income.

1. Take advantage of your property

Selling up and moving to a cheaper house may free up money to help fund your retirement. But keep in mind that it might affect your benefits if you’re receiving an age pension. Some of the proceeds from the sale might be counted as assessable under the age pension assets test, and this might lead to a drastic cut in your pension.

2. Supplement your income

Getting a part-time job could boost your cash flow if you are retired. But remember that working when you have become eligible for an age pension may reduce your pension amount. Discuss with your adviser how you might optimise your retirement benefits while working part time.

3. Rent out your property

If you have extra space in your home, you may consider to rent it out? Or if you have another property, like a holiday home, you may look into listing it as a short-term rental? This could impact the tax you pay when you sell your home so you should seek advice on these strategies.

4. Revisit your investments

Have you invested in securities? This may be a good time to meet with our financial adviser to review your portfolio. Your financial adviser may recommend strategies and ways to reduce your exposure to risk and volatility.

Understand the risks

You don’t have to be trapped in a situation where you are asset rich but cash poor. There are ways to boost your income, but keep in mind that some involve taking big risks. So seek financial advice to help you weigh your options and make decisions based on your situation.

We’re happy to help. Contact Dev Sarker today at 1300 71 71 36!

Social media could influence us to spend impulsively.

Can social media use be linked to spending? Research shows it can. For example, one study found that social networks such as Facebook and Instagram can motivate impulsive buying behaviours.[1]

But how does social media affect our spending?

1. Advertising

Sites like Facebook and Instagram have evolved from social networking platforms to powerful advertising tools. We only need to look at our social media feeds to realise how businesses use targeted advertising to expose us to brands, products and services. Targeted posts are effective at getting us to spend because they’re typically developed based on our demographics and even our behaviours.

2. Fear of missing out

Social media creates a tendency among users to compare their lifestyle to those of others. This comparison can trigger a fear of missing out or FOMO, leading us to buy and consume just to fulfil the urge to keep up with everyone else.

3. Encouraging imitation

Images of products or aspirational lifestyles posted on social media by people we respect or admire might influence us to spend unnecessarily or indulgently. This happens when we look to them for cues or guidance when we don’t know how to act and simply copy what they’re doing. Psychologists call this social proofing.[2]

4. Seamless shopping experience

Social media platforms can also encourage spending by providing a seamless shopping experience. For example, Facebook enables retailers to sell on the platform itself, and Instagram lets them add links to products and services mentioned in their posts so users can purchase them online. This makes it extremely easy to spend.

Making smart choices

Social media can help us make better choices by exposing us to more products and services and enabling us to learn about other people’s experiences using them. But it can also influence us to spend unnecessarily or impulsively.

By setting financial goals, you can make smart choices with your money. Your professional financial adviser can help you get started by creating a plan and budget to help you secure your financial future.