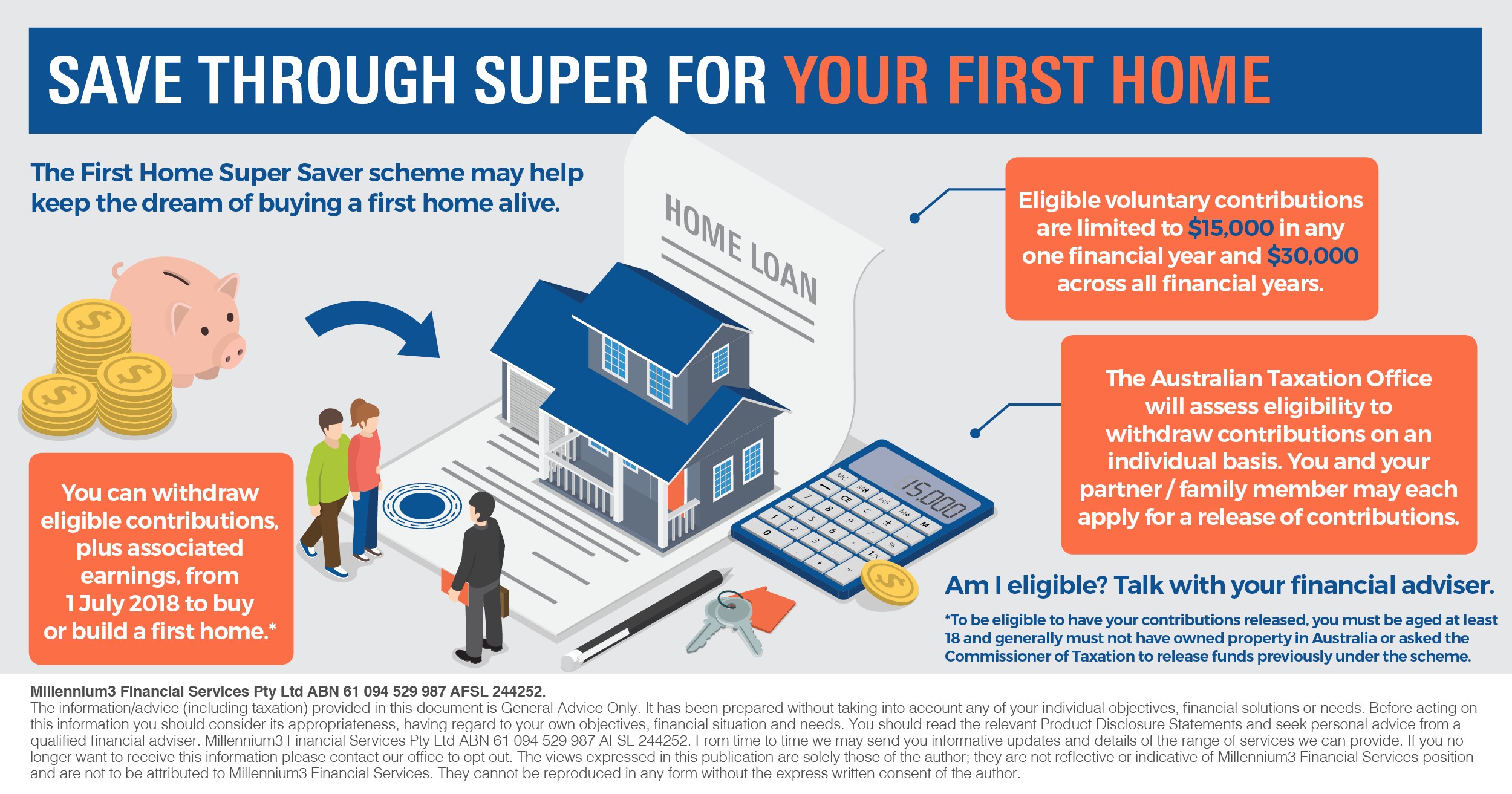

Options to consider when handling your spouses’ super when they pass away

- You can choose to take your spouse’s superannuation death benefit as a lump sum, a pension or a combination of both

- A lump sum can allow you to pay off debts, whereas a pension provides a regular income

- Take into account the different tax implications as it could affect your social security entitlements

When coping with the death of a loved one, the last thing you want to deal with is tough financial decisions. But if your husband or wife passes away, it’s good to be prepared in order to handle their super.

Depending on your financial situation, you may prefer to take your partner’s superannuation death benefit as a lump sum, an income stream or a combination of the two. Each option has its pros and cons, so you’ll need to work out which one provides an option more suitable for you. Here are some things to keep in mind.

Taking a lump sum

If you choose to take your spouse’s death benefit as a lump sum, you won’t have to pay any tax on it, regardless of your age or the age of your spouse when they passed away.

Taking your spouse’s death benefit as a lump sum is not only tax-effective, it also means you can use the money to pay off any debts — for example, your home, car, personal loans or credit cards.

Plus, if you take the benefit as a lump sum, you may be eligible for an anti-detriment payment from your spouse’s super fund. Basically, this is an additional benefit paid by the fund to offset the tax paid on your spouse’s super contributions. But check with your spouse’s fund first, as not all funds offer the anti-detriment payment ― and from 1 July 2017¹, it could be removed altogether.

Bear in mind though that if you’re over 65 and retired when you receive a lump sum death benefit, you won’t be able to reinvest it in super. It will also increase your assessable assets, which could affect your social security entitlements.

Keeping the money in super

As an alternative to taking a lump sum from super, you may be able to receive a death benefit pension. If you’re over 60 — or your spouse was over 60 when they died — your pension payments will be tax free.

If you’re under 60 and your spouse also dies before turning 60, the taxable component of the pension payment will be taxed at your marginal tax rate. You will also be entitled to a 15% tax offset. Keep in mind that choosing a pension means you won’t be eligible for the anti-detriment payment. On the upside, if you keep the money in super it will provide you with a regular income and continue to grow over time. Plus, it might have less of an impact on your social security entitlements than a lump sum benefit.

Weighing up your options

So which option is right for you? It depends entirely on your circumstances. Before making a decision, think carefully about your tax position, cash flow and the potential impact on your social security benefits.

Let’s take a look at Clare and Dominic, a retired couple in their late 60s who are both receiving a part Age Pension from Centrelink.

Clare has $400,000 in super, and draws $24,000 from her super each year as an account based pension. Clare commenced her pension prior to 1 January 2015 and retains the previous Centrelink treatment². The deductible amount on the pension is $24,000, which means none of the pension payment is assessed by Centrelink from this account based pension. Clare has nominated Dominic as a reversionary beneficiary, which means her account based pension will revert to Dominic if she dies.

Dominic also draws a $25,000 defined benefit pension from his own super each year. The couple, as homeowners, have $30,000 in savings, plus a car valued at $8,000 and home contents worth $10,000.

Sadly, Clare passes away and Dominic is faced with a decision. He can either:

- Continue receiving the account based pension.If Dominic keeps receiving Clare’s account based pension, it won’t affect his Centrelink entitlements. Based on his income and assets, he’ll still be eligible for an Age Pension of approximately $12,090 a year³. However, when the assets test changes on 1 January 2017, his Age Pension will be reduced to around $7,277⁴ a year.

- Take the death benefit as a lump sum. Dominic finds out that if he cashes in Clare’s $400,000 super balance, her fund will also pay an anti-detriment payment of $35,300. But this cash boost will also impact Dominic’s Centrelink benefits, reducing his Age Pension payments to $5,629 a year. And from 1 January 2017, these payments will be reduced to $4,972.

Choosing the lump sum option will give Dominic an extra $35,300 straight away — which will come in handy if he has substantial debts to cover. On the other hand, his Age Pension will be worth more each year if he hangs on to Clare’s account based pension.

In this case, Dominic needs to look at his short- and long-term financial goals to work out which option will be best for him overall.

A mix of both

The good news is that you don’t just have to choose one option or the other. With most super funds, you can receive your spouse’s death benefit as a combination of a lump sum and an income stream. So you might consider cashing in part of your spouse’s super and taking the remainder as an account based pension. That way you can pay off any outstanding debts and still have a stable income to fund your retirement.

Getting the appropriate advice

Rules around superannuation death benefits are complex, and it can be difficult to know which option is appropriate for you. Speak with a BlueRocke financial adviser to get expert guidance and make a difficult decision a little bit easier.

¹ In the 2016 Federal Budget, the Government has announced they will abolish anti-detriment payment effective from 1 July 2017. At the time of writing, this proposal has not been legislated.

² Account based pensions commenced prior to 1 January 2015 retain its previous treatment if the owner was in receipt of a Centrelink/DVA income support payment continuously since 31 December 2014.

₃ This amount is an annualised amount of fortnightly age pension payment of $465 and includes pension and energy supplement. Calculated based on Centrelink rates and thresholds current as at 1 July 2016.

₄ Estimated based on maximum pension entitlement as at 1 July 2016 and legislated lower asset threshold from 1 January 2017.