It may be easy to forget the 9.5% that is automatically paid by your employer into your super fund every pay check. However, it’s your money and will play an important role in your financial future. Your super should be one of the biggest assets you accumulate in your lifetime.

Additionally, super is a tax-effective way to save for your retirement period; which may be longer than you think.

Why should you care about super?

You’ll probably need more money than past generations to fund a longer retirement, with Australian life expectancies increasing all the time. And improvements to health care and living standards, your long retirement is also likely to be an active one.

Life expectancies at birth are currently 80.6 years for men and 84.1 for women[1]. The Australian Government Treasury’s recent Intergenerational Report projected that they’ll increase to 95.1 years for men and 96.5 years for women over the next 40 years.

This is where super comes in. It reduces the chance that you’ll need to rely on the Age Pension when you stop working.

How does super work?

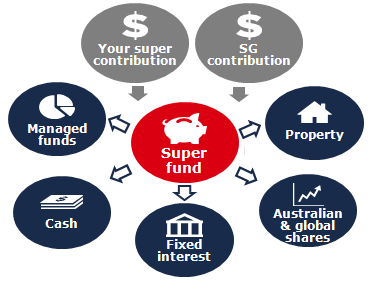

If you’re employed, your employer will generally make Super Guarantee (SG) contributions. This means that 9.5% of your salary goes straight into your super account – a fund that’s chosen by your employer or a fund of your choice.

Super funds will invest your money, together with the money of other members, in a range of investment types, also known as asset classes. The aim is to grow it over time.

How is super tax-effective?

All investment earnings within super are taxed at a maximum of only 15%, which is likely to be lower than your personal tax rate. This means your savings in super could grow faster than your savings outside of super, depending on how the investments within your super perform.

When can you access your super?

Even though it’s your money, you generally won’t be able access it until you retire after reaching your ‘preservation age’, which is between 55 and 60 depending on your date of birth.

In some extreme circumstances, you may be able to access your super before your preservation age. These include permanent incapacity, severe financial hardship and terminal medical conditions.

You can also have limited access to your super via a transition to retirement income stream once you reach your preservation age, even if you continue to work.

Do you have enough super to maintain your lifestyle in retirement?

The answer will depend on how long you will live for in retirement and the kind of retirement lifestyle you’re aiming for.

As a guide, the Association of Superannuation Funds of Australia (ASFA) regularly releases a Retirement Standard that breaks down how much retirees might need annually to fund ‘comfortable’ and ‘modest’ lifestyles. For the June 2015 quarter, the figures for a comfortable lifestyle are $42, 861 for singles and $58,784 for couples. This means that singles will need a lump sum of $545,000 at retirement and couples will need $640,000[2].

Want to know more?

Talk to a BlueRocke financial adviser, call us on 1300 71 71 36.

[1] Australian Government Actuary life tables

[2] Assumes 25 years of retirement from age 67. All figures in today’s dollars using 3.75% AWE as a deflator and an assumed investment earning rate of 7 per cent. They are based on the means test for the Age Pension in effect from 1 January 2017.