Click here to read the monthly eNewsletter exclusive for BlueRocke & SME Funding Hub clients:

https://bluerocke.com/wp-content/uploads/2023/12/SMEBlueRocke-Newsletter-Dec-23.pdf

Click here to read the monthly eNewsletter exclusive for BlueRocke & SME Funding Hub clients:

https://bluerocke.com/wp-content/uploads/2023/12/SMEBlueRocke-Newsletter-Dec-23.pdf

Click here to read the monthly eNewsletter exclusive for BlueRocke clients:

https://bluerocke.com/wp-content/uploads/2023/07/BlueRocke-July-Newsletter.pdf

Click here to read the monthly eNewsletter exclusive for BlueRocke clients:

https://bluerocke.com/wp-content/uploads/2023/04/BlueRocke-April-Newsletter.pdf

Here at BlueRocke we work with Accountants to support new Australians in their wealth creation. Over the past 10 years we have assisted Peter Chan and Andrew Wong at P&A Connect Accountants and Advisors with many of their clients who are busy medical professionals and business owners, around building and protecting their wealth using diverse long term investment and insurance strategies. This partnership means that clients’ wealth is built to levels higher than the would be on their own. They are reassured that they and their families are well provided for and can navigate the Australian financial systems better together.

With over 35 years Global financial experience and 10 years local knowledge, Dev Sarker can be your partner in assisting new Australians create wealth and keep clients for longer. Contact Dev today at https://bluerocke.com/

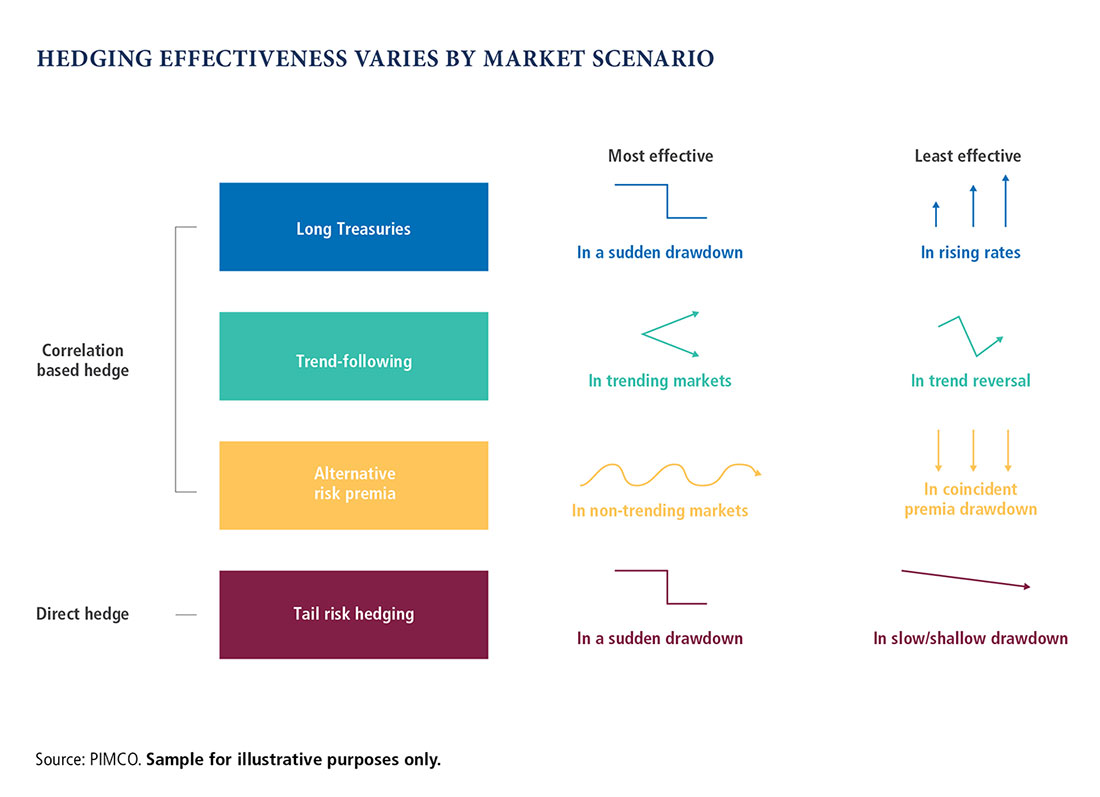

A look at specific strategies, and their trade-offs, for diversifying equity risk.

More investors are considering broadening their approach to diversifying equity risk to include strategies such as long duration bonds, managed futures, alternative risk premia, and tail risk hedging. However, it’s important for investors to know in what types of environments each strategy is more likely to work and in what environments each are likely to be less effective.

Not every type of risk-mitigating strategy can be expected to work in every type of market sell-off.

There is no “silver bullet” strategy to hedge an investor’s portfolio from risk events. We believe that investors should “diversify their diversifiers” by identifying the ideal blend of correlation-based hedges and outright hedges for their unique circumstances.

Source: PIMCO https://www.pimco.com.au/en-au/resources/education/hedging-for-different-market-scenarios

Learn how a diversified portfolio can be prepared for a number of economic scenarios.

A portfolio mix that combines both traditional and non-traditional asset classes – such as TIPS and commodities – may be better positioned for a number of potential economic and inflationary scenarios.

Stocks, bonds and cash, which form the core of many diversified portfolios, generally add value in some economic scenarios. In higher inflationary environments, assets such as emerging market securities, commodities and Treasury Inflation-Protected Securities (TIPS) may perform better.

Rounding out a core portfolio with non-traditional and real (inflation-hedging) assets can help investors participate in a broader range of economic environments while also managing volatility, which is particularly important in uncertain economic times.

Source: PIMCO https://www.pimco.com.au/en-au/resources/education/prepare-for-economic-changes-with-a-broader-allocation

If you have questions and would like your financial situation to be evaluated, please email us on ds@bluerocke.com with your contacts, for an exploratory meeting, at our cost, not yours.