The investment world can change dramatically from one month to the next. But these secrets of successful investors never go out of style.

Successful investing can be one of your biggest allies in the quest for long-term financial security. Unfortunately, unsuccessful investing can leave you wishing you’d kept your money in the bank.

So what are the secrets to making your investments achieve what you want them to achieve?

Here are some of the tactics used by successful investors around the world.

1. Start with a plan

Smart investors don’t just look for ‘good’ investments. They look for investments that will help them achieve specific goals.

You may be seeking a return above that available on cash or term deposits. In this case there are other investments such as shares and fixed income, which may be expected to generate higher returns than cash over the long term, however, they are also more volatile, so investors need to consider both the risk and return components of their portfolio.

2. Diversify widely

One of the main goals of investing may be to ensure you have a mix of assets that are likely to perform well at different times – helping you survive any downturn in a specific market or industry sector.

While many Australian investors are heavily exposed to Australian shares, a well-diversified portfolio will generally hold assets in each of the major asset classes (e.g. Australian and international shares, property, fixed income and cash).

3. Watch your costs

It’s easy to get fixated on the returns your investments can generate. But successful investors always keep track of, and seek to minimise, the fees and taxes associated with owning them.

A ‘buy and hold’ strategy can help you avoid transaction costs like brokerage, or buy and sell spreads from managed funds. It can also help you reduce capital gains tax, which generally decreases by 50% when you’ve held an asset for over 12 months.

4. Market Timing Risks

Attempting to time the market can be both difficult and dangerous to your portfolio. Market timing risks missing periods of strong performance, which can adversely impact a portfolio. Morningstar recently conducted a review of investment returns over 20 years, and determined that by being fully invested, investors generated a return of 8.7% p.a. However, the same investment that missed the top 10 returning days would have returned 6.1% p.a.

Despite periods of significant volatility on a daily basis, over the long term, investments in assets such as Australian Shares have generated strong returns.

5. Don’t panic

When share markets retreat (which they inevitably do), smart investors don’t hit the panic button and sell long-term investments based on short term volatility – this is made easier by following Step 1 “Start with a Plan”.

Instead, if you continue to invest during a market downturn, you may be able to buy high-quality investments at a lower price than you could if you waited for markets to recover.

Following the GFC, when the stock market bottomed in early 2009, many investors sold out of equities and held large proportions of cash in their portfolios. The opportunity cost of this decision has meant that some investors have missed a significant rally over the past decade.

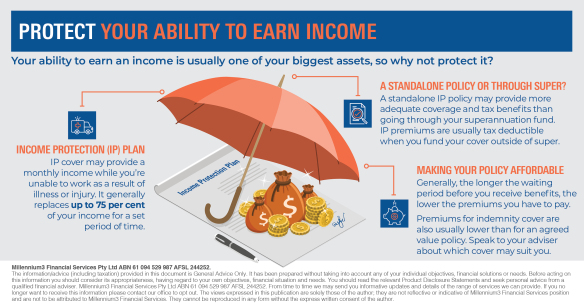

6. Protect your assets

Even a carefully constructed investment strategy can come unstuck if you need access to your money in an emergency.

A smart strategy is to ensure you maintain a sizeable cash reserve, and put in place appropriate insurance such as income, TPD and life insurance. Having appropriate insurances in place can help prevent the need for a ‘fire sale’ of your investments if you suffer a serious illness or accident.

Tip: Income protection typically replaces up to 75% of your income if you can’t work due to an illness or accident.