Don’t let an illness stop you from looking after your finances.

A Financial Adviser could work with you to develop a financial plan that’s specifically tailored to your needs, so get in touch with Dev Sarker today on 1300 71 71 36.

Don’t let an illness stop you from looking after your finances.

A Financial Adviser could work with you to develop a financial plan that’s specifically tailored to your needs, so get in touch with Dev Sarker today on 1300 71 71 36.

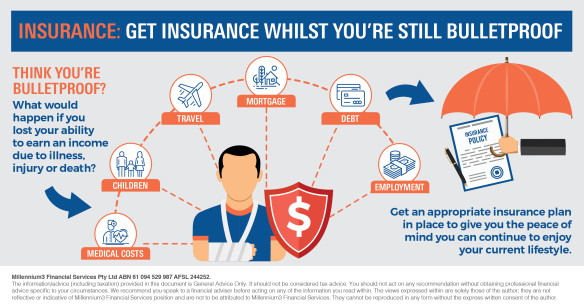

According to research by TAL insurance provider the cost of personal insurance soars after the age of 35. This is also the time in our lives that you may be going through significant change such as marriage, children, a bigger mortgage and more responsibilities.

In the previous 5 years to 2017, TAL paid out insurance claims to the sum of $66m to people

aged up to 35, but this figure soared for those aged 35 – 46 to a total payout sum of $152m.

From our experience working with clients and insurance providers, it’s wise to get a personal insurance cover in place before you turn 35. If you are approaching your 35th birthday now is the ideal time to think about this, but it is important to stress that an appropriate insurance plan is wise

at any age.

It’s time to get some professional advice – from an adviser with the technical expertise and experience required to make sure you’re properly covered.

But before you make such an arrangement, it is wise to get professional advice on how it works. Your financial adviser may talk you through the rules of spouse contributions and the requirements

to become eligible for a tax offset.

Speak to Dev Sarker today on 1300 71 71 36!

We all like a good cost saving tip, even if it is something we already know, it never hurts to revisit some top tips and take a look at our current situation to see if there are savings to be made.

Any little savings we make throughout the year can be diverted to a bigger savings pool such as an investment portfolio or term deposit to help build wealth over time.

If you are not completely aware of what you have in your super fund and how it is performing now is the time to do a quick investigation. Having one fund, instead of multiple funds may save you on fees. Being with a top performing fund rather than a default fund could mean a higher return on your investment, which really adds up over time. Making sure you are only paying for what you need is important, if you are paying for insurance when you have a separate insurance policy this could be an expense you get rid of. However, there is not a one size fits all approach, which is why tailored financial advice could help to find a super solution that suits your individual circumstances.

This is a good way to reduce your taxable income and boost your super. Some of your pay is diverted to your super fund, hence reducing your taxable income, and this money is taxed within the super fund at only 15%. The other benefit of course is that it boosts your super fund and with the power of compound interest over time you can set yourself up for a nice retirement lifestyle.

Reviewing your utility costs each year can be a great way to make little savings add up. By reviewing the contracts you are on, asking the provider for a better deal or getting onto a pay-on-time contract that offers a discount are simple ways you can save on utilities. Consider ways you can be smarter with your utilities at home – buy energy efficient appliances, turn of lights when you are not using them, take shorter showers, install a water tank, be conscious of your use of utilities.

Whilst you don’t want to deny yourself too many little luxuries or conveniences, looking at your levels of consumption could expose some cost savings. Consider walking or taking public transport rather than driving everywhere, only buy what you need at the grocery store rather than stockpiling, reduce the number of times you eat out or buy coffees by one less a week, don’t rotate your wardrobe items until you have worn out existing items, take advantage of free activities in your local area such as the library, beach, bushwalks which will connect you with the community and save money on entertainment.

A professional financial adviser can help you with cash flow and budgeting and then help you divert your savings into a vehicle that will start making you some money. Get in touch with Dev Sarker today on 1300 71 71 36.

Are you affected by the increase in the Age Pension’s qualifying age? Take steps now to avoid getting caught short on retirement income.

The minimum age to qualify for the Age Pension has started going up. For those born on or after 1 July 1952, the qualifying age increases by six months every two years until it reaches 67 in July 2023. It rises to 66 in July this year.

So if you’re turning 45 this year and plan to retire when you reach 60, you will need to wait until you’re 67 before you can apply for the Age Pension. You’ll have to rely on your own savings and super in the interim, making it crucial to ensure you have enough money put away for later years. But the good news is that there’s still time to grow your retirement savings.

Contributing more to your super can be a reliable route to bolstering your retirement fund. By making extra contributions through salary sacrifice, you can grow your super and at the same time reduce the amount of income tax you pay. The government will tax your salary sacrificed contributions at 15 per cent, which could be much lower than your marginal tax rate.

Making non-concessional or after-tax contributions is another option. You can contribute up to $100,000 each financial year if your total superannuation balance is less than $1.6 million. To understand how these contributions work, it’s wise to get professional advice.

Your personal savings can supplement your super payments in retirement. But are they growing enough now to provide you with some income when you retire?

To build up your savings, you may have to invest part of it and make sure it’s growing faster than the rate of inflation. Investing in a managed fund or buying an investment bond may help you increase your nest egg, but you should seek professional advice to see if these instruments are appropriate for you.

Besides the Age Pension, you may be eligible for other government benefits and concessions. The Seniors Card, for example, offers individuals over the age of 60 discounts on some commercial and public services. Concessions that allow you to buy prescription medicine at a discount are also available.

But keep in mind that these benefits have strict eligibility rules. There’s also no guarantee that these entitlements will still be available by the time you retire. So take charge of your retirement. By working with your financial adviser, you can develop a strategy that helps ensure you’ll be well provided for regardless of changes to pension policies.

Setting a financial goal for the New Year? Take

steps to make

it work.

It’s that time of year when we set new goals or dust off old ones. But how can we boost our chances of sticking to our financial resolution? Here are some practical tips.

It’s good to be ambitious, but you may have a better chance of adhering to your resolution if you have a smaller, reachable goal. Using the well-established SMART formula can help. SMART stands for:

Create a plan that can help you take small but

regular steps toward reaching your financial goal.

The key is to set specific milestones and a timeframe for each. You may wish to

talk to your financial adviser about setting a plan for your financial

situation and goal.

Tell your family members or friends about your resolution, or post it on social media. By making your resolution known to others, you might feel more responsible for sticking to it.

Record and analyse your progress against your milestones. It could help to get your financial adviser to check your progress every so often.

Enjoying the process of reaching your goal may help you stick to your financial resolution. So give yourself a small reward every time you hit a milestone.

Whether you want to boost your savings or retirement fund, your financial adviser may be able to help you stay on track to achieve your resolution.