Boost your super with the work test exemption

If you’re a recent retiree and looking to increase your superannuation savings, here’s some good news for you.

The Australian Government is proposing to make it easier for recent retirees to save more super by allowing them to contribute for a year without having to show that they’ve been ‘gainfully employed’.

The current rules

Currently, anyone below 65 can contribute to their super regardless of whether they work or not. But those aged between 65 and 74 need to meet the work test before they can make super contributions. To pass the test, they have to show that they’ve been gainfully employed for at least 40 hours over 30 consecutive days in the financial year they plan to contribute.

The government has already given members with a total super balance of less than $500,000 some flexibility to further grow their super. These individuals can carry forward any unused amount below the concessional contribution cap of $25,000 on a rolling basis for five years starting from 1 July 2018. They can use their unused cap amounts from 1 July 2019. But people between 65 and 74 must still meet the work test before they can make these ‘catch up’ contributions.

The proposed measure

Now, to encourage this age group to save more for retirement, the government is proposing to give individuals who don’t meet the work test an extra year to beef up their super savings. From 1 July 2019, those aged between 65 and 74 with a super balance below $300,000 will be able to make voluntary contributions in the first financial year that they don’t satisfy the work test requirement. Once eligible, they don’t have to remain under the $300,000 balance cap during the 12 month period.

The annual concessional and non-concessional contributions caps will continue to apply, but members can access any unused concessional contributions cap amounts they have carried forward.

The government will assess total super balances at 30 June of the financial year in which members last met the work test. So those who retire in the 2018–19 financial year may be eligible to make additional contributions.

Seek professional advice

If you’re considering contributing to your super under the proposed work test exemption, it may be wise to speak to your adviser to see how making additional super contributions may work to your advantage.

Speak to Dev Sarker today on 1300 71 71 36!

Hindsight Bias

Introduction

After an event has occurred, people often look back and convince themselves that the outcome was obvious and likely, and that they could have predicted it. This is known as ‘hindsight bias’, or the ‘knew-it-all-along’ effect. In actual fact – particularly in the investment world – outcomes can rarely be reasonably predicted ahead of time.

Hindsight bias is common and can be attributed to our natural need to find order in the world. We create explanations that allow us to make sense of our surroundings, and that help us to believe that events are predictable.

The human ability to find patterns and to link cause and effect can be useful – for example, to a scientist carrying out experiments. However, finding false links between an event and its outcome can sometimes result in unreliable over-simplification.

Studies[1] have also shown that hindsight bias occurs because it’s easier for people to understand and remember the actual outcome than it is to consider the many other possible outcomes that, in the end, didn’t come to pass.

Given how important investment decisions are in our everyday lives, hindsight bias is frequently observed among investors.

Impact on investment decisions

One of the most significant effects of hindsight bias is the way in which it can influence investment decisions.

It does this by encouraging investors to over-estimate the accuracy of their past forecasts. This leads to a false sense of security, causing investors to assume that their future forecasts and decisions will be equally accurate.

As a result, investors often make decisions based on future investment outcomes which may seem obvious and highly likely to them, but actually involve much more uncertainty and risk than they realise.

Philip E. Tetlock, a professor of management at the Wharton School of the University of Pennsylvania, has studied people’s tendency to exhibit hindsight bias. “Even after it has been explained to you 100 times, you can still fall prey to the bias” he has said. “Indeed, even after you’ve written about it 100 times.”

The ability of investors to identify a bubble after it has burst is a classic case of hindsight bias. In both 1999 and 2007, for example, very few investors correctly forecasted that stock markets were about to fall. However, when we now look back at those times, it’s often felt that the signs of what would happen next were clear and there for all to see.

Case study

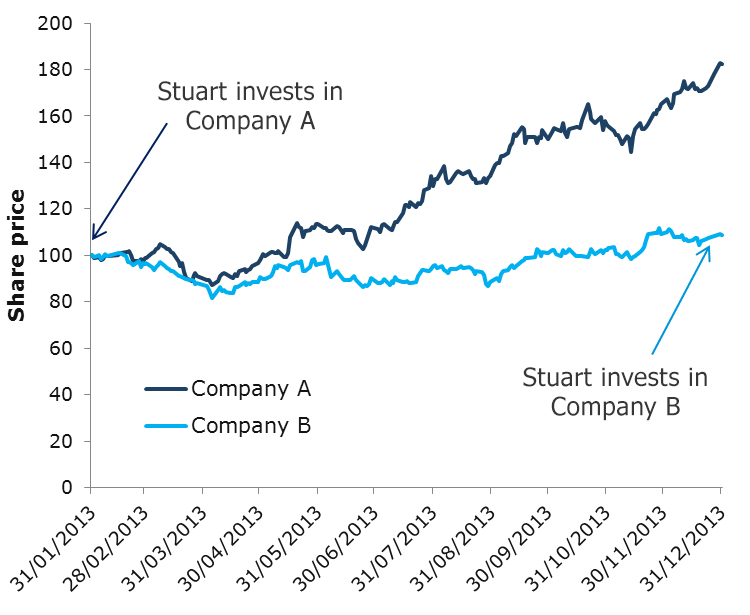

Hindsight bias can be illustrated by the following case study and chart. In this example, our investor Stuart invests in two stocks during 2013.

In January, after much research, Stuart decides to invest in Company A. The share price soon increases substantially in value. Stuart is delighted – his research has paid off! He congratulates himself on his perception and investment insight.

In December, Stuart decides to invest again. His success with Company A gives him confidence that he will be able to pick another winning stock. This time, Stuart invests in Company B.

Of course nobody can be certain how Company B’s shares will perform, including Stuart. But he is more confident in his expected (positive) outcome for Company B – and less focused on the wide range of other possible investment outcomes for its share price – than he might have been before his success with Company A.

In short, hindsight bias has led Stuart to become over-confident in his stock-picking skills.

Illustrative purposes only.

Eliminating hindsight bias

The first rule of avoiding the common investment pitfalls associated with hindsight bias is to be aware that it exists.

Even experienced investors can never be certain how particular investments will perform in the future. Investors must always balance risk and return, placing equal emphasis on all factors that have impacted previous investment decisions, both successful and unsuccessful.

Doing so will provide investors with a clearer and more balanced perspective to their decision-making process. Maintaining this focus can enable investors to avoid the unfounded over-confidence in their predictive abilities that hindsight bias can trigger.

An alternative approach would be to invest in a managed fund, run by a professional investment manager. Investment managers tend to follow consistent, repeatable investment processes which can help eliminate hindsight bias from investment decisions.%

The Power of Compounding

Compounding isn’t a new concept – many of us will remember studying it back in our school days. Legendary scientist Albert Einstein famously called it ‘the most powerful force in the universe’, while American business magnate John D Rockefeller suggested compounding is the ‘eighth wonder of the world’.

These might sound like bold claims, but the power of compounding on an investment portfolio should certainly not be underestimated.

What is compounding?

In simple terms, compounding is the process whereby returns made on an investment are reinvested in order to generate subsequent returns of their own.

The concept of compounding is best illustrated using an example. Twins Annie and Vanessa both allocated $10,000 to the same interest-bearing investment on their 25th birthday. For simplicity, let’s assume the investment pays interest of 5% per year.

Annie reinvests all of her interest every year, while Vanessa banks the $500 each year and spends it on everyday living expenses. Let’s see how their investments had fared by their 45th birthdays.

Figure 1: Effect of compounding over 20 years

| Annie’s investment value ($) | 5% compound interest ($) | Vanessa’s investment value ($) | 5% interest ($) | |

| 10,000 | 10,000 | |||

| Year 1 | 10,500 | 500 | 10,000 | 500 |

| Year 2 | 11,025 | 525 | 10,000 | 500 |

| Year 3 | 11,576 | 551 | 10,000 | 500 |

| Year 4 | 12,155 | 579 | 10,000 | 500 |

| Year 5 | 12,763 | 608 | 10,000 | 500 |

| Year 6 | 13,401 | 638 | 10,000 | 500 |

| Year 7 | 14,071 | 670 | 10,000 | 500 |

| Year 8 | 14,775 | 704 | 10,000 | 500 |

| Year 9 | 15,513 | 739 | 10,000 | 500 |

| Year 10 | 16,289 | 776 | 10,000 | 500 |

| Year 11 | 17,103 | 814 | 10,000 | 500 |

| Year 12 | 17,959 | 855 | 10,000 | 500 |

| Year 13 | 18,856 | 898 | 10,000 | 500 |

| Year 14 | 19,799 | 943 | 10,000 | 500 |

| Year 15 | 20,789 | 990 | 10,000 | 500 |

| Year 16 | 21,829 | 1,039 | 10,000 | 500 |

| Year 17 | 22,920 | 1,091 | 10,000 | 500 |

| Year 18 | 24,066 | 1,146 | 10,000 | 500 |

| Year 19 | 25,270 | 1,203 | 10,000 | 500 |

| Year 20 | 26,533 | 1,263 | 10,000 | 500 |

| Total value received | 26,533 | 20,000 | ||

Source: CFSGAM. Figures used for illustrative purposes only.

Vanessa earned $500 interest each and every year for the 20 year period – a total of $10,000. Of course she still had her original $10,000 investment as well.

Annie, on the other hand, saw her investment grow to more than $26,000 by reinvesting her interest. The additional $6,000 she earned over and above Vanessa highlights the power of compounding. You can see from the table that Annie’s investment is now earning her $1,263 per year, while Vanessa’s investment is still earning her only $500. This differential would continue to grow over time if the sisters remained invested.

Make compounding work even harder for you

The power of compounding can be magnified if you make small regular contributions to your investment. Let’s look at another example to highlight the concept.

Brothers Jim, Dan and Tom all decided to invest $10,000 in the same managed fund for 10 years. Over that time the fund returned an average of 8% pa.

Happy with his original investment decision, Jim did not make any additional contributions. Dan, the wiser brother,understood the effects of compounding and made additional regular savings of $100 per month. Tom – the wisest of them all – worked out he could afford to save an extra $200 per month and made sure he always contributed that amount to his investment. The difference in their investment returns over 10 years is startling:

Figure 3: Effect of compounding with regular contributions over 10 years

| Initial investment | Monthly contribution | Annual return | Value after 10 years | |

| Jim | $10,000 | 0 | 8% pa | $21,589 |

| Dan | $10,000 | $100 | 8% pa | $39,602 |

| Tom | $10,000 | $200 | 8% pa | $57,614 |

Source: CFSGAM. Figures used for illustrative purposes only.

Of course the example is a stylised one. It ignores potential fluctuations in investment returns over the period, which would affect the three outcomes in reality.

These examples highlight how compounding and contributing regularly to an investment can have a major influence on investment performance. The long-term performance impact of compounding can be significant and must not be overlooked by investors. This is also the main reason why it pays to engage with your super early and start making additional contributions so compounding can work it’s magic. Perhaps Einstein and Rockefeller were right, after all.

Herd behaviour

Herd behaviour is driven by emotional rather than rational behaviour. Often little attention is paid to investment fundamentals as investors focus on what other people are reacting to in the market.

All investors are prone to behaviours and emotions that can lead to poor investment decisions. One of the most common pitfalls is known as ‘herd behaviour’. This describes large numbers of individuals acting in the same way at the same time, typically by buying into rising markets and selling out of falling markets. This behaviour can cause markets to dramatically rise and fall in value – known as ‘bubbles’.

Bubbles can only be identified with hindsight, after a rapid and marked drop in value has occurred. These sudden drops are sometimes referred to as ‘crashes’ or ‘bubble bursts’. Because bubbles are only identified in retrospect, many investors often get caught out by the sudden and rapid decline in the value of their investment.

Herd behaviour is driven by emotional rather than rational behaviour. These emotions are typically optimism and greed when markets are rising, and fear and panic when markets are falling. Little attention is paid to the investment fundamentals, which means herd behaviour rarely leads to successful investment outcomes.

There are two main drivers of herd behaviour when it comes to investing. Firstly, people don’t want to miss out on making a profit. Secondly, we assume that when a large number of people are buying into the same investment, they can’t all be wrong. This means that there is often little understanding of the underlying investment, and more attention is focused on what other people are doing. Consequently, it is often the less experienced investor who gets caught up in herd behaviour.

Bubble indicators – what to watch out for

- Strong, sustained rallies and stretched valuations

- Hearing ‘this time it’s different’

- A flurry of initial public offerings, mergers and acquisitions

- Investor greed and a fear of missing out

- Everything moving together, regardless of quality

- Media headlines talking up the latest investment trend

Case study

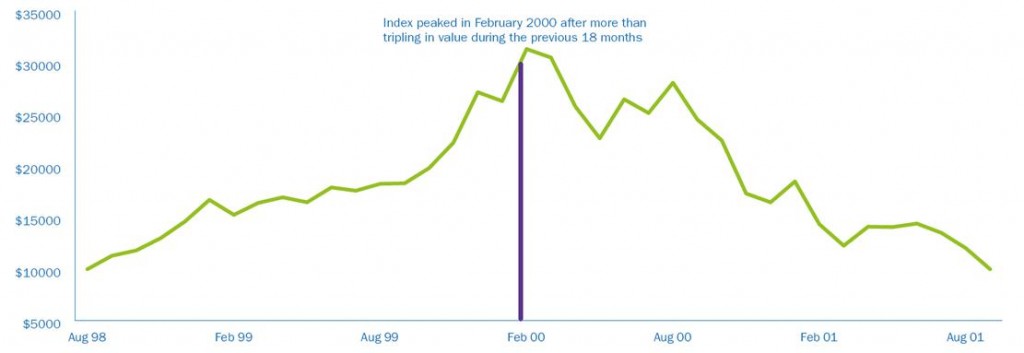

It’s October 1999 and Ken has been keeping an eye on the sharemarket. Everyone is talking about the exciting future of technology companies and he has noticed most of them have doubled in value during the past 12 months. He doesn’t know much about investing or technology companies, but assumes all the other investors know something that he doesn’t. Without really understanding why the stocks are rising, he invests $10,000 in a technology-based index fund, reassured that many other investors are doing the same. Four months later he is delighted that the value of his investment has risen more than 50%. All those people were right after all.

Then, in February 2000, his investment starts losing value and Ken can’t see any reason behind the fall. All of a sudden everyone is rushing to sell their technology stocks and no one is buying any; the exact opposite of just a few weeks earlier. The drop in value is so abrupt that by the time Ken reacts and sells his holdings he has lost most of his original investment.

Like many others who had jumped on the ‘dot.com’ bandwagon, Ken did not do his research and invested without fully understanding the sector or risks. He thought to himself “this time it’s different”. Looking back he acknowledges that the signs of a bubble were there for all to see.

One way to avoid such a pitfall is to invest in a well diversified investment portfolio with a disciplined investment process which is designed to meet long-term investment goals, rather than be concerned with following the latest trend.

Exhibit 1: Value of $10,000 invested in the technology-based NASDAQ stock market (three years to 31 August 2001)

Source: Bloomberg. Chart is used for illustrative purposes only.

While it’s tempting to follow the latest investment trend, it is imperative to always fully understand an investment before making an investment decision.

Feel free to contact me if you have any questions about herd behaviour.

“Be greedy when others are fearful and fearful when others are greedy” – Warren Buffet

Cashed Up

When cash is king, choose the best option for you.

Hoarding your dollars under the mattress probably won’t have much appeal for many of us. But is it possible you may be doing the modern day equivalent with your current cash investments.

The reason the mattress isn’t such an attractive idea is that, apart from the obvious security issues, the value of your stash falls over time. You earn no interest and there’s no capital growth.

There could be a similar result if you don’t think through the options available for cash investments. It may mean lost opportunities and fail to maximise the returns from your most liquid assets.

Which account?

While the everyday bank account will always score highly as a convenient place to park your cash, it comes at a price.

A better option for your cash reserves could be a high-interest savings account. Here, your cash can be earning more than a typical transaction account.

A slightly higher rate of interest again can be earned in a term deposit. In return for agreeing to tie up your cash for a set period of time, usually between a month and five years, you’ll earn more. The longer the period, the higher the interest. Term deposit accounts often require a minimum amount of around $1,000 to $5,000.

You’ll need to be certain that you won’t need the money for the fixed term because withdrawing funds early can attract penalties. Also, don’t forget to keep track of when the term expires so that you can plan what to do next. Unwittingly allowing the term deposit to rollover into another term might not be best for your circumstances at the time.

Of course, there are many other ways to hold cash investments, such as managed funds that either focus purely on cash investments, or include a large holding of cash investments as part of their portfolio.

What suits you?

Another way to take advantage of the security and performance of cash and fixed interest is to change the asset allocation in your superannuation or pension fund.

You can manipulate your investments inside your fund to create a portfolio that suits the market conditions and your own goals.