Are current market events a repeat of the Global Financial Crisis in 2008?

Current market volatility is distinctly different to the GFC. For one, banks will be part of the solution this time, not the problem. Portfolio Manager, Myooran Mahalingam discusses in this video.

We’re here to help you understand what happens in a share market downturn,

If you’ve seen a decrease to your super balance as a result of the coronavirus, it’s understandably cause for concern.

When your balance goes down (or up), it’s as a result of changes in the value of investments in your super fund — this could be a mix of cash, shares, fixed income, property, and more—and, of course, your balance will change when you or your employer adds money each month, or when you withdraw money in retirement or through insurance premiums, fees and taxes.

Severe as they can feel, events like this aren’t permanent. In fact, based on history, markets have bounced back from other global shocks including epidemics like SARS and Swine Flu.

In this article, we’ll address five key areas to consider when it comes to thinking about your super in a market downturn and when there’s increased volatility.

1. Maintain a long-term perspective

Super is like any type of investment, there will be times of highs and lows. For the majority of Australians, super may be our longest-term investment given we start investing in super when we get our first job and don’t access the money until retirement.

It’s also the nature of investment markets to change rapidly, particularly shares, property or fixed income investments. The share market for example, is a public market so when the share market rises or falls, changes in share prices may impact the value of your super if it’s invested in shares.

Markets recover with time

But from what we’ve seen in the past with events that disrupt investment markets, markets do eventually recover, it just takes time.

From the 1987 Stock Market Crash to the bursting of the Tech Bubble in 2000, each trigger is different and the time it takes to recover varies too — it can take months, weeks or even years. While disruptions to markets occur fairly regularly, they are impossible to accurately predict.

So, if you do decide to make changes to your investments during falling markets—like switching to a different type of portfolio—it’s important to also consider what impact that will have on your returns when markets recover.

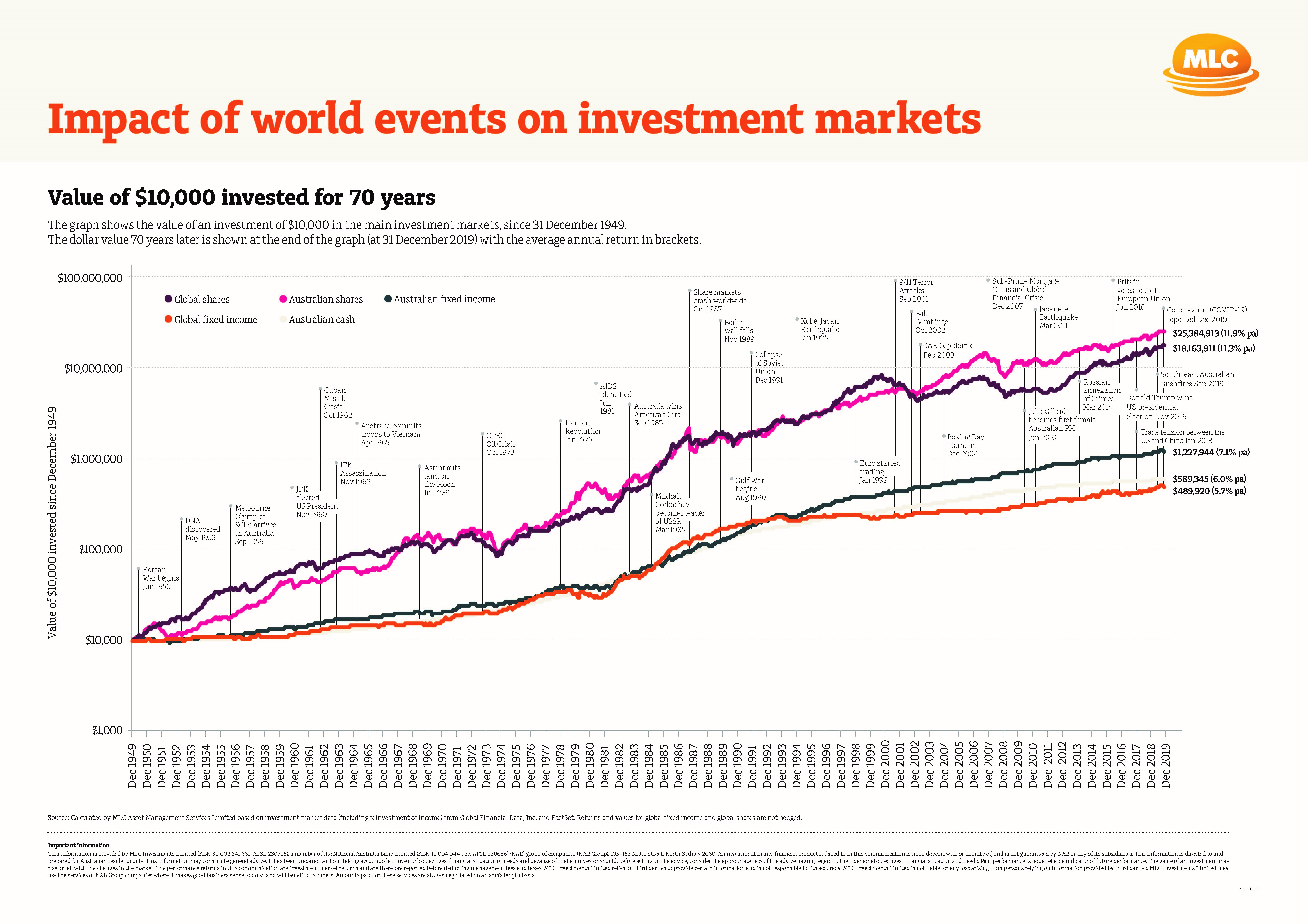

The value of $10,000 invested for 70 years

The dollar value 70 years later is shown at the end of the graph (at 31 December 2019) with the average annual return in brackets.

2. Review your investment strategy

While these events may make you want to take action, it’s important to take a moment to consider your investment strategy including why you invested that way in the first place.

Understanding the investments that make up your strategy and how they are expected to perform over long periods of time, can help you think about your strategy objectively, instead of reactively. Particularly short-term market volatility which can influence your investment decisions.

If your strategy is intended to be a long-term plan, which may be the case for those with a long way to go before they retire, making decisions based on short-term market fluctuations may greatly affect whether you achieve your long-term goals.

If you’re approaching or are in retirement, it’s still important to stay focused on your investment strategy. Carefully consider all of your options, and their impact on your retirement goals, before making any significant changes. Speaking to a financial adviser may help with this.

3. Be aware of your risk tolerance

It’s always important to consider how you feel about risk and market volatility.

By understanding your risk tolerance, you’ll be better able to make decisions about the structure of your investment portfolio in a way that aligns to you personally. Risk tolerance depends on how you feel about taking risk and your ability to do so, such as whether you are financially able to bear the risk.

Asset classes like shares and property, have higher return potential and experience greater fluctuations in value, than cash or fixed income investments. How much exposure you choose to have in each of these asset classes, may change depending on your level of comfort, especially during periods of investment market instability.

4. Consider diversification

One of the most effective ways of reducing the impacts of investment fluctuations is to diversify. Multi-asset or diversified funds invest across multiple asset classes to assist in reducing volatility.

Diversification essentially follows the concept of not putting all your eggs in one basket by spreading your money across many asset classes, countries, industries, companies, and even investment managers.

When one area of your portfolio is weak and falling, another may be rising strongly. If you have money invested across many areas, changes in their values tend to balance each other out.

Diversification doesn’t mean you can avoid negative returns altogether, but it helps reduce the size and frequency of fluctuations in your portfolio. Particularly compared to if you’d only invested in shares, for instance.

5. Seek support from a professional

Super funds have lots of information available online to help you understand your savings.

Working with a financial adviser can help you design a plan to achieve your financial goals. They may also provide you with a better understanding about the risks and rewards of investing and how you can manage risk.

While the impact of market volatility can affect your super, it’s important to remember it won’t last forever. The investment strategy you adopt should take into account factors including—your financial goals and the savings required to get there, the number of years you have to invest, the return you can expect from your investments, and how comfortable you are with volatility.

We are help to help. Contact Dev Sarker at 1300 717 136 today.

Important Update – The Government’s new super and pension provisions announced 22 March

Over the weekend, the Australian Government announced its economic support package to help Australians who are under financial stress as a result of the Coronavirus.

Two of the support measures announced include the early release of superannuation for those financially affected by the Coronavirus and a temporary reduction of minimum pension payment requirements for retirees.

A summary of these measures, including information about who is eligible and how individuals can access these provisions can be found in this link – https://www.mlc.com.au/personal/corona-virus/government-superannuation-changes

If you need more information, we are happy to help. Contact Dev Sarker today at 1300 717 136.

Also known as ‘salary continuance insurance’ or ‘disability income insurance’, income protection provides a portion of your income, for example 75% of your annual salary, if you are unable to work due to injury or sickness for a certain period of time. You need to advise your annual salary when you take out the cover.

Income protection policies always have a waiting period and a payment period. The waiting period is the time you must wait from when you make a valid claim, to the time you become eligible to start receiving payments. The payment period is the period you can be paid so long as you remain unable to work. Other terms and conditions apply depending on the policy. All of these factors affect the level of premiums you pay.

What are the changes?

Recently, the Australian Prudential Regulation Authority (APRA) announced that it is concerned that insurance companies have been keeping premiums at unsustainably low levels to compete for customers. APRA also think that some policies have very generous features and terms that, in some cases, provide a financial disincentive for people to return to work after successfully making a claim.

Has APRA announced what changes will be made?

Yes, effective from 31 March 2020, insurance companies must:

stop providing ‘agreed value’ policies that are based on the income you advise at the start of cover, regardless of any subsequent change in income. This means no more ‘agreed value’ contracts can be bought or sold after 31 March 2020.

What other changes are likely to be made?

Other changes, effective from 1 July 2021, include:

your insured income is to be based on your annual income at the time you make a claim, and are not able to look back more than 12 months

limits of 100% of income replacement payments can be made in the first six months and 75% thereafter, with a total limit of $30,000 per month

a maximum payment period of five years, with a right to renew cover

insurance providers must have adequate risk management processes in place to mitigate the risks associated with long term benefit payment periods.

APRA is seeking feedback on the above changes from the industry by 29 February 2020 and will make a final decision by 30 June 2020.

What happens to existing policies?

If you have an existing retail income protection policy which include a ‘Guarantee of Renewability’ in the policy wording, that is, the policy is automatically renewed each year, your policy will continue.

Are policies which meet APRA’s new expectations available now?

No, to purchase an income protection policy which takes into account APRA’s changes we need to wait until the insurance providers have issued new policies with new Product Disclosure Statements.

More information

For more information, please read APRA’s media release or contact our financial adviser, Dev Sarker today at 1300 71 71 36.

If you want to get ahead, financially, it’s necessary to take some steps to get there. It may seem daunting and overwhelming but like anything, if you have a professional guiding you along the way, small steps can lead to something great.

Step 1 | Seek advice

It’s hard to achieve great success without a team of experts behind you and your wealth is no different. Getting professional financial advice means your adviser can work through a myriad of options with you and implement a strategy aligned closely to your financial goals. Retirement planning, tax-effective super strategies, investments and estate planning? Your financial adviser can help.

Step 2 | Understand what role risk plays

One of the first things your financial adviser will do is work out your risk profile, which they will check at regular review meetings. Why? Because risk is related to return, and this will help drive the recommendations they make to you in terms of your financial plan. Generally, the higher the risk, the higher the return. While some people like higher risk investments because they have the potential to deliver higher returns, others prefer less risky investments. It’s important to remember that markets are cyclical and shares are a long-term investment so if the market wobbles, your financial adviser is best placed to keep an eye on your investments and determine if they remain aligned to your overall financial strategy.

Step 3 | Check your super

Your superannuation could be your largest asset, other than your own home. Given it’s such a large sum that you have been contributing to for years and years, and you are relying on it to sustain you in your retirement, isn’t it something you want to get right? Sure, it’s a long-term investment, but it’s important that it is invested in-line with your risk profile and financial goals. And you DO have options. As well as your employer contribution, you can kick in a bit extra through salary sacrificing. Contributing more to super will not only boost your account balance, it could reduce the amount of tax you pay.

Step 4 | Stick to a budget

Sounds boring, right? But a budget is not boring, it’s empowering!! Setting a realistic budget helps you understand where your money is going, what can be trimmed and where you can invest to save for your future. Understanding your overall financial health and having a budget aligned to your financial goals gives you a real understanding of the benefits of working with a financial adviser. You can start to see a real change in your circumstances. Having a budget doesn’t mean giving up things you want, it just means you plan for them and you make sure you can afford them BEFORE you spend the money. Setting and sticking to a budget is really the simplest way to help you get ahead.

Need advice? We’re happy to help. Call 1300 71 71 36 to speak to a financial adviser today!